環境光センサの世界市場(2025-2034):センサ種類別(フォトダイオード型、CMOS型、赤外線型)、出力種類別、取り付けスタイル別

※本ページの内容は、英文レポートの概要および目次を日本語に自動翻訳したものです。最終レポートの内容と異なる場合があります。英文レポートの詳細および購入方法につきましては、お問い合わせください。

*** 本調査レポートに関するお問い合わせ ***

世界の環境光センサー市場は、2024年には9億2610万米ドルとなり、2034年には年平均成長率11.1%で26億米ドルに達すると予測されています。環境光センサー産業の成長は、ADAS機能のために家電や自動車アプリケーションでこれらのセンサーの採用が増加していることなどの要因によるものです。

スマートフォン、ラップトップ、タブレット、スマートTVの急速な普及は、世界的な環境光センサ需要を牽引する要因の1つです。環境光センシング機能は、最新のスマートフォン、ノートパソコン、スマートテレビ、その他の民生用電子機器に搭載される機能として、顧客からますます求められるようになっています。デバイスのバッテリー寿命の向上、プレミアムなユーザーエクスペリエンス、より快適な視聴体験に対する需要の高まりが、消費者向けデバイスへの環境光センサーの採用を促進しています。

Statistaによると、2023年には世界で13億3,000万台のスマートフォンが出荷され、2024年のスマートフォン市場は7.8%成長しました。同様に、スマートTVの保有台数は2026年までに11億台に達すると予想されており、環境光センサーの売上を大きく押し上げるでしょう。メーカーがユーザーエクスペリエンスの向上、バッテリー寿命の延長、画面対ボディ比の最大化を継続的に目指しているため、ディスプレイの端から端までの画面サイズを最大化し、ディスプレイの下でセンサーを動作させることができる環境光センサーの需要は拡大するでしょう。

マルチカラー検出機能を備えた超薄型(0.3mm以下)環境光センサーへの投資は、大手家電メーカーとの契約獲得に大きなチャンスをもたらすと予想されます。

環境光センサーは、アダプティブ・ヘッドライト・コントロール、ダッシュボードの自動輝度調整、自動調光IRVM、アニメーション・ターン・インジケーターなどの高度な機能を実現し、ドライバーの快適性を高め、視認性を向上させ、車内体験を全体的に向上させる上で極めて重要な役割を果たすため、自動車アプリケーションで高い支持を得ています。アンビエントLED照明は、自動車メーカーにとって重要なデザイン上の差別化要素となっています。

アメリカ高速道路交通安全局Highway Loss Data Instituteによると、アメリカでは2027年までにアダプティブ・ヘッドライトを搭載した車両が14%に増加する見込みで、環境光センサーの大きな成長機会を示しています。既存の自動車OEMは、最新モデルや高級モデルで広範囲に環境照明を提供しており、予測期間中の環境光センサの需要を促進しています。

今後予定されているEuro NCAP 2025+のアダプティブ・ドライビング・ビーム・システムの要件を満たすため、車載グレードの環境光センサー・ソリューションの開発に注力することで、センサーメーカーは大手自動車OEMと長期的なパートナーシップを確立し、ヨーロッパで大きな市場シェアを獲得できる可能性があります。

さらに、自然光と人工光を区別する機械学習機能を備えたマルチスペクトル環境光センサーの開発により、緊急ブレーキや歩行者検知などのアプリケーションに新たな機会が生まれる可能性があります。

環境光センサーの市場動向

環境光センサー業界の主要トレンドの1つは、エネルギー効率を促進する政府規制の増加で、スマート照明の採用を促進しています。例えば、2021年1月、国際基準審議会は、周囲光レベル、占有率、時間イベントの3つの入力に基づいて、使用していないときに照明を自動的に消灯または下げることによりエネルギー使用量を削減することを目的とした国際省エネルギーコード(IECC)を発表しました。

環境光センサーにより、スマート照明システムは、昼間の自然光で十分な場合に照明を調光または消灯することができ、大幅なコスト削減につながります。この自動調光は、省エネと電気代の削減に役立ち、スマート照明システムの費用対効果の高いソリューションとなります。

スマートホームやスマートビルで、照明スイッチを作動させたり、自然光に応じて明るさを調整したりして人工照明を調整し、エネルギー効率を促進するスマート照明の採用が増加していることが、予測期間中の環境光センサーの成長を促進します。

産業用アプリケーションへの環境光センサーの採用も、環境光センサー市場の成長を支える大きな傾向です。産業オートメーションでは、環境光センサーは、時間帯や自然光の条件に基づいて適応的なワークスペース照明を作成するために使用されます。

環境光センサーは、安全侵害や装置の問題によって引き起こされた可能性のある低照度や高照度の事例を追跡することで、作業空間の安全性を向上させるために使用されます。品質および検査アプリケーションでは、環境光センサーは色の選別と検出に使用されます。これらのセンサーは、さまざまな物体から反射される光を正確に測定し、さまざまな色を区別することができるため、物体の検出や選別を行うことができます。より広い波長検出機能を備えたカスタム設計の環境光センサーソリューションは、産業オートメーションアプリケーションのセンサーメーカーに新たな収益機会をもたらす可能性があります。

環境光センサー市場分析

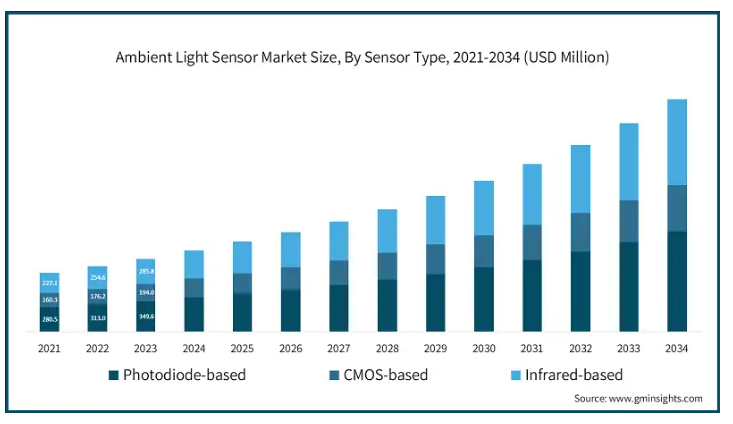

センサの種類別では、フォトダイオードベース、CMOSベース、赤外線ベースに分類。

フォトダイオードベースのセンサー市場は、2023年に3億4960万米ドル。フォトダイオードは、光を効果的に電気信号に変換するため、家電や自動車産業で採用が多く、高い人気を集めています。フォトダイオードベースのセンサーは、消費電力要件がそれほど厳しくないアプリケーションにコスト効率の高いソリューションを提供。

赤外線ベースセンサ市場は、2022年に2億5460万米ドル。この市場のシェアが高いのは、製品識別や偽造品検出用のカラーコードリーダー、スマートビルや温室の照明制御などのアプリケーションで赤外線ベースの環境光センサの採用が増加しているため。

CMOSベースセンサ市場は、2021年に1億6,030万米ドル。COMSベースの環境光センサーは、スマートフォンや車載アプリケーションへの統合により大きく成長。これらのセンサーは、その改善されたセンシング能力と小型化されたフォームファクタにより、非常に使用されています。

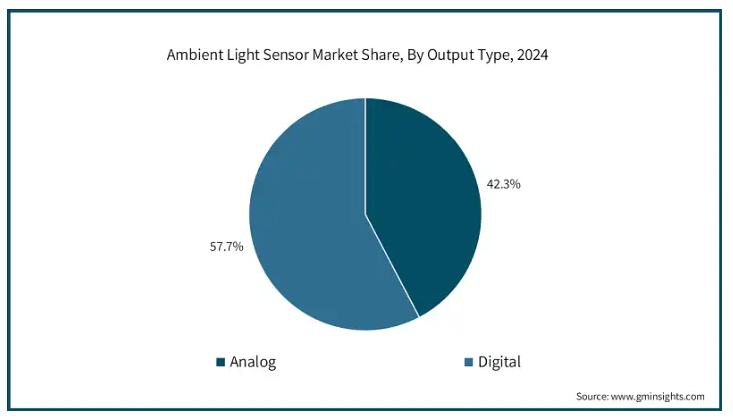

出力タイプ別では、環境光センサー市場はアナログとデジタルに分けられます。デジタル環境光センサーは、スマートフォンやテレビにアダプティブ・ディスプレイを求める購買層が多いため、電子機器や自動車での採用が増加しています。ワークスペースでは、人間中心の照明が大きな支持を集めており、デジタル環境光センサーが生産性向上のための明るさの最適化に役立っています。

デジタル出力タイプ市場は、絶え間ない技術開発、スマート装置の需要急増、省エネ・スマート照明ソリューションの重視の高まりにより、2024年には世界の環境光センサ市場の42.3%を占める見込み。

アナログ出力市場は、2024年に世界の環境光センサー市場の57.5%を占める見込み。処理遅延を最小限に抑えた光センシングにおける低遅延応答、簡素化された設計と電磁干渉への耐性、少ない製造コストなどの要因が、予測期間中の市場成長を支えています。

環境光センサー市場は、実装スタイルに基づいてSMD/SMT、スルーホール、その他に区分されます。装置の小型化・薄型化への急速なシフトが、環境光センサにおけるSMD/SMTフォームファクタの需要を増加させています。

SMD/SMT市場は、2024年に6億7,190万米ドルを占め、市場を支配。このセグメントの大きなシェアは、電子装置の小型化傾向の高まり、センサ技術の進歩による信頼性と精度の高いSMD/SMT実装環境光センサの開発促進など、いくつかの要因によるもの。

スルーホール市場は、2023年に1億8420万米ドル。このセグメントの成長は、高い耐久性、優れた放熱性、産業用および自動車用アプリケーションにおける信頼性が原動力。これらのセンサーは過酷な条件にも耐えられるため、屋外照明、スマート街灯などのアプリケーションに最適。

環境光センサー市場は、集積度によりディスクリートとコンビネーションに区分されます。コンビネーションインテグレーション市場は、予測期間中にCAGR 14.3%で成長すると予測されています。このセグメントの高成長は、リアルタイムで低遅延の環境センシングのためにAIプロセッサと環境光センサを統合する需要の増加が原動力となっています。

ディスクリート統合は、信頼性の向上と高精度を提供し、近接センシングやディスプレイの輝度調整など、精密な光センシングを必要とするアプリケーションに適しています。

コンビネーション・インテグレーション・セグメントは、予測期間中にCAGR 14.3%で成長する見込みです。スマート装置やモノのインターネット(IoT)の普及が進み、車載用途の需要が急増することで、この分野は拡大する可能性があります。

アプリケーション別に見ると、環境光センサー市場は、家電、自動車、産業、ホームオートメーション、ヘルスケア、エンターテインメント、セキュリティ、その他に二分されます。アダプティブ輝度制御、より良いカラーコントラストと精度への要求、ブルーライト低減などのトレンドが、民生用電子機器における環境光センサの成長を促進しています。

民生用電子機器市場は、OLEDやAMOLEDのような新しいディスプレイ技術の開発とともに、スマートフォンやタブレットの採用が増加しているため、2024年には3億1150万米ドルを占め、市場を支配。

2024年、自動車市場は1億9370万米ドル。自動車への環境光センサーの採用は、先進運転支援システム(ADAS)や車内照明の強化などの先進機能に対する顧客の需要を後押ししています。

ホームオートメーション市場は、予測期間中に最も高い成長を記録する見込みで、2025~2034年のCAGRは14.5%。このセグメントの高成長は、エネルギー効率とエネルギー料金の削減を目的としたスマート照明ソリューションへの環境光センサーの統合が増加していることに起因しています。

産業用市場は、2034年に3億2790万米ドルに達する見込み。これは、製品の品質管理や色検知に基づく選別に環境光センサの採用が増加していることなどが要因。

ヘルスケア市場は、2034年までに1億8,240万米ドルに達すると予測されています。ヘルスケアアプリケーションにおける環境光センサの成長を支える装置は、概日照明システムにおけるこれらのセンサの採用の増加、心拍数や酸素飽和度測定のための光電式(PPG)センサを強化するためのウェアラブル医療機器における環境光センサの統合の増加。

エンターテイメント市場は、予測期間中にCAGR 9.3%で成長すると予測されています。エンターテインメント分野の成長を支えているのは、より没入感のある体験を実現するためのゲーム用AR/VR装置における環境光センサの普及拡大。

セキュリティ市場は、2023年に4070万米ドル。エネルギー効率を維持しながら、照度の低い公共エリアの安全性を高め、駐車スペースの安全性を高めるためにスマート街灯に環境光センサの採用が増加していることが、市場成長を支える主な要因。

2024年には、北米が世界の環境光センサー市場で31%の最大シェアを占めました。この市場の大きなシェアは、この地域の大規模な自動車、製造拠点、エネルギー効率に対する厳しい政府政策、スマートシティプロジェクトの採用増加によるもの。

2024年、アメリカの環境光センサ市場は2億2250万米ドル。米国環境光センサ市場は、スマート照明の開発重視の高まり、電子機器採用の急増、自動車産業の急成長によって牽引される可能性が高い。

カナダ環境光センサ市場は、2034年に1億6920万米ドルに達する見込み。カナダの環境光センサー市場を牽引しているのは、強力なエネルギー効率規制、環境・社会・ガバナンス(ESG)基準に準拠するためのスマート照明システムへの環境光センサーの統合、都市照明の自動化を推進するためのトロントやバンクーバーのスマートシティプロジェクトにおけるスマート街灯への環境光センサーの導入といった要因。

2024年、ヨーロッパは世界環境光センサ市場の22%を占めました。ヨーロッパの環境光センサの成長を支える要因は、ADASと自律走行車の業界をリードする研究開発のパイオニアがいる自動車製造ハブが確立していること、安全で安心な公共の場に対する需要が増加していること、精密農業に環境光センサが採用されていること。

ドイツの環境光センサ市場は、2034年までに2億3,270万米ドルに達する見込み。ドイツにおける環境光センサーの成長は、主要自動車メーカーがアダプティブヘッドライト、室内照明などの機能のために環境光センサーを統合したことに起因しています。さらに、EUのエネルギー効率指令も、省エネを目的としたスマートビルへの環境光センサの採用を後押ししています。

英国の環境光センサー市場は、予測期間中にCAGR 10.3%で成長する見込み。英国市場は、スマートシティの急速な発展と環境光センサー技術の継続的な進歩によって支えられています。環境光センサーは、交通量の少ない時間帯の照明の減光に使用されるほか、人が通行する際に暗い場所を照らすことでセキュリティを向上させます。

フランスの環境光センサー市場は、2025年から2034年にかけて年平均成長率11.6%で成長する見込み。フランスには多くの多国籍ブティック店や高級レストランが存在します。これらの店舗は、贅沢でパーソナライズされた顧客体験を提供しようと常に努力しています。

フランスの環境光センサ市場は、ブティック店、高級ホテル、レストランで、時間帯や顧客の好みに応じて雰囲気を調整するセンサの採用が増加していることが牽引しています。

イタリアの環境光センサー市場は、2034年までに6,110万米ドルに達する見込み。イタリアの環境光センサー市場は、老人ホーム、病院、高齢者介護施設における概日照明システムでの採用が増加していることが要因。

スペインの環境光センサ市場は、2034年に4680万米ドルに達すると予測。スペインにおける環境光センサーの成長は、次世代電気自動車や自律走行車へのALSの統合が進んでいることに起因しています。さらに、ブドウやオリーブの栽培を制御するための栽培灯を調整するための環境光センサの採用も市場成長を支えています。

2024年、アジア太平洋地域は世界の環境光センサー市場の29%を占めています。この地域には大手電子機器ブランドが存在し、装置にプレミアム機能とユーザーエクスペリエンスを求める顧客層が多いことが、この地域の市場成長を支えています。

中国の環境光センサー市場は、予測期間中にCAGR 13.7%で成長する見込み。中国には主要な自動車メーカーの拠点があり、これが市場拡大を支えています。国際貿易局(ITA)によると、中国は年間販売台数、生産台数ともに世界最大の自動車市場です。2025年には、国内生産台数は約3,500万台になると予想されています。

中国には大規模な電子機器製造エコシステムが存在し、スマートホーム技術へのシフトも環境光センサーの需要に貢献しています。

日本は、アジア太平洋地域の環境光センサー市場で22.8%のシェアを占める見込みです。日本の大手電子機器ブランドは、画面の明るさをダイナミックに調整するために、テレビ、ゲーム用モニター、プロジェクターなどの家電製品に環境光センサーを組み込んでいます。

韓国の環境光センサー市場は、予測期間中にCAGR 10.8%で成長する見込み。サムスンやLGディスプレイなど韓国の主要ディスプレイメーカーは、OLED、QD-OLED、MicroLEDパネルなどの先進ディスプレイや、サムスンの折りたたみ式携帯電話(Galaxy Z Fold、Z Flip)などのスマートフォンに環境光センサーを搭載しています。

インドの環境光センサー市場は、予測期間中に13.5%のCAGRで最も高い成長が見込まれています。インドは、格安スマートフォンとミッドレンジスマートフォンの最大市場です。また、インドはウェアラブル市場としても成長しています。これらの電子機器では、ダイナミックな輝度調整にALSが使用されています。インドにおけるこれらの電子機器の高い普及率が、環境光センサーの市場成長を支えています。

ANZの環境光センサー市場は予測期間中CAGR 11.5%で成長する見込み。ANZにおける環境光センサーの採用は、スマートインフラの進歩、エネルギー効率規制、電気自動車の採用増加によって支えられています。

2024年、ラテンアメリカは環境光センサの世界市場で7%のシェアを獲得。精密農業における環境光センサの採用率の高さが、同地域における環境光センサの成長要因。

ブラジル環境光センサ市場は、予測期間中CAGR 6.7%で成長する見込み。ブラジルの環境光センサ市場の成長は、作物収量向上とエネルギー消費削減のための光調節を改善する精密農業ソリューションの成長に起因。

メキシコの環境光センサー市場は予測期間中CAGR 8%で成長する見込み。メキシコのアンビエントライト市場の成長は、スマートシティ構想の採用が増加していることに起因。メキシコ当局は、エネルギー消費を削減し持続可能性を高めるために、街灯に環境光センサーを統合しています。

2024年、中東とアフリカは、世界の環境光センサ市場の9%のシェアを占めています。公共インフラにおける持続可能性とエネルギー効率、自動化への推進力の高まりが市場成長の主な要因。

2024年、UAEは中東・アフリカの環境光センサー市場の45.9%を占めています。UAE環境光センサ市場の成長は、スマートシティ、エネルギー効率化技術、持続可能な開発で世界的リーダーになろうとする政府の追求が原動力。

サウジアラビアの環境光センサー市場は予測期間中CAGR 8.9%で成長する見込み。サウジアラビアの環境光センサーは、二酸化炭素排出量の削減とエネルギー効率の向上を目指すサウジアラビアのグリーンイニシアチブが原動力。公共インフラにおける照明自動化強化のためのALS採用が政府のエネルギー効率目標をサポートし、市場成長を促進。

南アフリカの環境光センサー市場は2034年までに1700万米ドルに達する見込み。小売業や広告業におけるデジタルサイネージへの環境光センサーの採用拡大が、予測期間中の南アフリカ市場成長を牽引。

環境光センサー市場シェア

アンビエントライトセンサー市場は、既存グローバルプレーヤーだけでなく、ローカルプレーヤーや新興企業も存在するため、競争が激しく、非常に断片化されています。世界の環境光市場の上位5社は、ams-OSRAM AG、Melexis NV、オン・セミコンダクター、シャープ、ローム半導体で、合計で35%のシェアを占めています。これらの企業は、エネルギー効率を高め、IoT装置とシームレスに相互作用する高度なセンサーを提供することで、市場で競争しています。例えば、2024年6月、アンビエント照明用車載LEDドライバのメーカーであるMelexisは、LIN RGB製品portfoilioをMLX81123で拡張すると発表しました。スリープモードでは、MLX81123のスタンバイ消費電流はわずか25 µAで、28 Vのジャンプスタートが可能です。動作温度は-40℃~+125℃と広く、温度監視用の温度センサーを内蔵しているため、最も要求の厳しい車載アプリケーションにも最適です。

新製品投入は、市場の主要企業が市場シェア拡大のために採用している最も重要な戦略的展開です。主要な環境光センサーメーカーは、自動車分野での普及を目指し、新製品の発売を増やしています。例えば、ams-osram AGは2023年、次世代乗用車に組み込むためのインテリジェントな環境光センシング機能を備えたOSIRE® E3731i LEDを発売しました。同社はまた、LED、マイコン、センサーなどの互換性のある装置が標準シリアルバス上で相互に通信できるようにする「言語」である、新しいオープンシステムプロトコル(OSP)を作成しました。OSPはどのメーカーも無料で使用でき、製品およびサプライヤーの活気あるエコシステムを育成し、アンビエント照明分野における自動車OEMの技術開発イニシアチブを支援します。

ams-OSRAM AGは、環境光の強度を正確に測定し、人間の目の光に対する反応と一致させる環境光センサーを提供しています。例えば、2024年12月、オスラムはValeoと提携し、光学部品、電子機器、ソフトウェアからなるアンビエント照明システムを開発しました。

Melexis NVは主に、顧客の要求と業界のニーズの進化に対応した迅速な製品開発で市場をリードしています。

オン・セミコンダクターは、さまざまなアプリケーション向けに幅広い環境光センシング製品を提供しています。このような膨大な製品ポートフォリオにより、オン・セミコンダクターは市場で主導的な地位を占めています。

環境光センサー市場の企業

環境光センサー業界の上位5社は以下の通りです:

The global ambient light sensor market was valued at USD 926.1 million in 2024 and is estimated to grow at a CAGR of 11.1% to reach USD 2.6 billion by 2034. The growth of the ambient light sensor industry is attributed to factors such as increasing increased adoption of these sensors in consumer electronics and automotive application for ADAS features.

The rapid proliferation of smartphone, laptops, tablets, and smart TVs is one of the leading factor driving the demand for ambient light sensor worldwide. Ambient light sensing capabilities are increasingly becoming a sought-after feature by customers in latest smartphones, laptops, smart TVs and other consumer electronic devices, allowing the device to adjust screen brightness as per the natural light condition around the device. The increasing demand for enhanced device’s battery life, premium user experience, and more comfortable viewing experience are driving the adoption of ambient light sensors in consumer devices.

According to Statista, in 2023, 1.33 billion smartphones were shipped worldwide, and the market of smartphones grew by 7.8% in 2024 indicating a significant growth potential for ambient light sensors in smartphones. Similarly, smart TV ownership is expected to reach 1.1 billion units by 2026 which will significantly drive the sales of ambient light sensor. As manufacturers continuously aim to improve the user experience, increase battery life, and maximize screen-to-body ratios, the demand for ambient light sensors will grow as they enable maximum edge-to-edge display screen size – with sensor operation under the display.

Investments in ultra-thin (sub 0.3mm) ambient light sensors with multi-colour detection capabilities are anticipated to open up significant future opportunities for securing contracts with leading consumer electronics manufacturers.

Ambient light sensor is gaining high traction in automotive applications as they play a pivotal role in enabling advanced features such as adaptive headlight controls, and automatic dashboard brightness adjustments, auto-dimming IRVMs, animated turn indicators etc., enhancing driver comfort, improving visibility, and elevating the overall in-car experience. Ambient LED lighting has become a key design differentiation feature for automotive manufacturers.

According to Highway Loss Data Institute, National Highway Traffic Safety Administration, U.S., the number of vehicles enabled with adaptive headlights in the U.S. is expected to increase to 14% by 2027 showcasing significant growth opportunities for ambient light sensors. Established automotive OEMs are providing ambient lighting extensively across their latest and luxury models, driving the demand of ambient light sensors during the forecast period.

Focusing on developing automotive grade-ambient light sensors solutions to meet the upcoming Euro NCAP 2025+ requirements for adaptive driving beam systems could enable sensor manufacturers to establish long-term partnerships with leading automotive OEMs and gain significant market share in Europe.

Additionally, the development of multi-spectral ambient light sensors with machine learning capabilities to distinguish between natural and artificial lights could open up new opportunities in applications such as emergency braking and pedestrian detection.

Ambient Light Sensor Market Trends

One of the key trends in the ambient light sensor industry is the increasing government regulations promoting energy efficiency, driving the adoption of smart lighting. For instance, in January 2021, the International Code Council released the International Energy Conservation Code (IECC) with an aim to reduce energy use by automatically turning off or lowering lighting when it is not in use based on three inputs: ambient light level, occupancy, or a time event.

Ambient light sensors enable smart lighting systems to dim or turn off lights when natural daylight suffices, leading to significant cost savings. This automatic dimming helps save energy and lowers electricity bills, making it a cost-effective solution for smart lighting systems.

The increasing adoption of smart lighting to help smart homes and buildings regulate artificial lighting by activating light switches or adjusting brightness in response to natural light for promoting energy efficiency will propel the growth of ambient light sensors during the forecast period.

The adoption of ambient light sensors for industrial applications is another major trend supporting the growth of ambient light sensors market. In industrial automation, ambient light sensors are used to create adaptive workspace lighting based on time of day and natural light conditions.

Ambient light sensors are used for improving the workspace safety by tracking instances of low or high light intensities, which may have caused due to safety infringement or a problem with the equipment. In quality and inspection applications, ambient light sensors are used for colour sorting and detection. These sensors can accurately measure the light reflected from various objects and differentiate between various colors, enabling them to detect and sort objects. Custom designed ambient light sensor solutions with wider wavelength detection capabilities could open up new revenue opportunities for sensor manufacturers in industrial automation applications.

Ambient Light Sensor Market Analysis

Based on the sensor type, the market is segmented into photodiode-based, CMOS-based, and infrared-based.

Photodiode-based sensor market accounted for USD 349.6 million in 2023. Photodiodes are gaining high popularity because of their high adoption in the consumer electronics and automotive industries as it effectively converting light into an electrical signal. Photodiode-based sensors offer a cost-effective solution for applications with less stringent power consumption requirements.

Infrared-based sensor market accounted for USD 254.6 million in 2022. The higher share of this market is attributed to increasing adoption of infrared-based ambient light sensors in applications such as color code reader for product identification and counterfeit detection, lighting controls in smart buildings and greenhouses.

CMOS-based sensors market accounted for USD 160.3 million in 2021. COMS-based ambient light sensors are experiencing significant growth due to integration in smartphones, and automotive applications. These sensors are highly used due to their improved sensing capabilities and reduced form factor.

Based on output type, the ambient light sensor market is divided into analog and digital. Digital ambient light sensors are increasingly adopted in consumer electronics and automotive as buyers seek adaptive displays in smartphones and TVs. Human-centric lighting is gaining significant traction in workspaces where digital ambient light sensors help optimize brightness for increasing productivity.

The digital output type market is expected to account for 42.3% of the global ambient light sensors market in 2024 owing to the constant technological developments, surge in demand for smart devices, and growing emphasis on energy-saving and smart lighting solutions.

The analog output market is expected to account for 57.5% of the global ambient light sensors market in 2024. Factors such as low-latency response in light sensing with minimal processing delays, simplified design and resistance to electromagnetic interferences, and less production cost are supporting the market growth during the forecast period.

Based on mounting style, the ambient light sensor market is segmented into SMD/SMT, through hole, and others. The rapid shift towards smaller and thinner devices are increasing the demand for SMD/SMT form factors in ambient light sensors.

The SMD/SMT market dominated the market accounting for USD 671.9 million in 2024. The large share of this segment is attributed to several factors such as the rising trend of miniaturization of electronic devices, as well as growing advancements in sensor technology facilitate the advancements of reliable and accurate SMD/SMT mounted ambient light sensors.

The through hole market accounted for USD 184.2 million in 2023. The growth of this segment is driven by high durability, superior heat dissipation, and reliability in industrial and automotive applications. These sensors can withstand harsh conditions make them ideal for applications in outdoor lighting, smart streetlights etc.

Based on integration, the ambient light sensor market is segmented into discrete and combination. The combination integration market is projected to grow at a CAGR of 14.3% during the forecast period. The high growth of this segment is driven by increasing demand for integration of AI processors with ambient light sensors for real-time, low-latency environmental sensing.

Discrete integration offers improved reliability and high accuracy that is suitable for applications that need precise light sensing including proximity sensing and display brightness adjustment.

The combination integration segment will grow at a CAGR of 14.3% during the forecast period. Rising proliferation of smart devices and the Internet of Things (IoT), as well as surge in demand for automotive applications is presenting lucrative growth potential for segment expansion.

Based on application, the ambient light sensor market is bifurcated into consumer electronics, automotive, industrial, home automation, healthcare, entertainment, security, and others. Trends such as adaptive brightness control, demand for better colour contrast and accuracy, blue light reduction etc. are propelling the growth of ambient light sensors in consumer electronics.

The consumer electronics market dominated the market, accounting for USD 311.5 million in 2024 owing to the increase in adoption of smartphones and tablets, along with the rise in development of novel display technologies like OLED and AMOLED.

In 2024, the automotive market accounted for USD 193.7 million. The adoption of ambient light sensors in automotive is driven customer demand for advanced features such as advanced driver assistance systems (ADAS), and enhanced interior lighting.

The home automation market is expected to register highest growth during the forecast period, growing at a CAGR of 14.5% for 2025 to 2034. The high growth of this segment is attributed to increasing integration of ambient light sensors in smart lighting solutions for energy efficiency and reduction in energy bills.

The industrial market is expected to reach USD 327.9 million by 2034, owing to factors such as increased adoption of ambient light sensors for product quality control and sorting based on colour detection.

The healthcare market is projected to reach USD 182.4 million by 2034. Factors supporting the growth of ambient light sensors in healthcare applications are increased adoption of these sensors in circadian lighting systems, increasing integration of ambient light sensors in wearable medical devices to enhance photoplethysmography (PPG) sensors for heart rate and oxygen saturation measurements.

The entertainment market is projected to grow at a CAGR of 9.3% during the forecast period. The growth of entertainment segment is supported by increased proliferation of ambient light sensors in gaming AR/VR devices for more immersive experience.

The security market accounted for USD 40.7 million in 2023. The increased adoption of ambient light sensors in smart streetlights for increasing safety of less illuminated public areas and increasing safety of parking spaces while maintaining energy efficiency is the major factor supporting market growth.

In 2024, North America accounted for the largest share of 31% of global ambient light sensor market. The large share of this market is attributed to the large automotive, manufacturing hubs in the region, stringent government policies for energy efficiency, and increased adoption of smart cities projects.

In 2024, the U.S. ambient light sensors market accounted for USD 222.5 million. United States ambient light sensors market is likely to be driven by the growing emphasis on the development of the smart lighting, surge in adoption of consumer electronics, as well as rapid growth of the automotive industry.

The Canada ambient light sensors market is expected to reach USD 169.2 million by 2034. The market for Canada ambient light sensors is driven by factors such as strong energy efficiency regulations, integration of ambient light sensors in smart lighting systems to comply with environment, social, governance (ESG) standards, and deployment of ambient light sensors in smart streetlights across smart cities projects in Toronto and Vancouver for driving urban lighting automation.

In 2024, Europe accounted for a share of 22% of global ambient light sensor market. Factors supporting growth of ambient light sensors in Europe are established automotive manufacturing hub with industry leading research development pioneers in ADAS and autonomous vehicles, increased demand for safe and secure public places, and adoption of ambient light sensors in precision agriculture.

The Germany ambient light sensors market is expected to reach USD 232.7 million by 2034. The growth of ambient light sensors in Germany is attributed to the integration of ambient light sensors by leading automotive manufacturers for features such as adaptive headlight, interior lighting etc. Moreover, the EU energy efficiency directives are also supporting the adoption of ambient light sensors in smart buildings for energy saving.

The UK ambient light sensors market is expected to grow at a CAGR of 10.3% during the forecast period. The UK market is bolstered by the rapid development of smart cities and continuous advancements in Ambient light sensor technology. Ambient light sensors are used to dimming lights during low traffic hours, along with improving security by lighting dark areas when people are passing.

France ambient light sensors market is expected to grow at a CAGR of 11.6% from 2025 to 2034. France has a strong presence of many multinational boutiques stores and high-end restaurants. These stores are constantly striving to provide a luxurious and personalized customer experience.

The market of ambient light sensors in France is driven by the increasing adoption of these sensors in boutique stores, high-end hotels and restaurants, adjusting ambience based on time of the day and customer preferences.

Italy ambient light sensors market is expected to reach USD 61.1 million by 2034. The market for ambient light sensors in Italy is driven by increasing adoption of these sensors in circadian lighting systems in nursing homes, hospitals, and elderly care facilities.

Spain ambient light sensors market is projected to reach USD 46.8 million by 2034. The growth of ambient light sensors in Spain is attributed to the increasing integration of ALS in next-generation electric vehicles and autonomous vehicles. Moreover, the adoption of ambient light sensors to regulate grow lights for controlled cultivation of grape and olive cultivation is also supporting the market growth.

In 2024, Asia Pacific accounted for a share of 29% of global ambient light sensor market. The presence of leading consumer electronics brands in the region coupled with a large customer base demanding premium features and user experiences in devices are supporting the market growth in the region.

The China ambient light sensors market is expected to grow at a CAGR of 13.7% during the forecast period. China has one of the major automotive manufacturers bases that is supporting the market expansion. According to the International Trade Administration (ITA), China is the largest automobile market in the world in terms of both yearly sales and manufacturing output. By 2025, it is anticipated that domestic production will account for around 35 million vehicles.

The presence of large electronics manufacturing ecosystem in China, as well as shift towards smart home technologies is also contributing to the demand of the ambient light sensor.

Japan is expected to account for a share of 22.8% of the ambient light sensors market in Asia Pacific. The leading electronics brands in Japan are integrating ambient light sensors in consumer electronics such as TVs, gaming monitors, and projectors for dynamic adjustment of screen brightness.

South Korea ambient light sensors market is expected to grow at a CAGR of 10.8% during the forecast period. The major display manufacturers in South Korea such as Samsung and LG display are integrating ambient light sensors in advanced displays such as OLED, QD-OLED, and MicroLED panels and smartphones such as Samsung’s foldable phones (Galaxy Z Fold, Z Flip).

Ambient light sensor market in India is expected to grow at a highest CAGR of 13.5% during the forecast period. India is the largest market for budget smartphones and mid-range smartphones. India is also a growing market for wearables. These consumer electronics devices uses ALS for dynamic brightness adjustment. The high adoption of these consumer electronics in India is supporting the market growth of ambient light sensors.

Ambient light sensors market in ANZ is expected to grow at a CAGR of 11.5% during the forecast period. The adoption of ambient light sensors in ANZ is supported by increasing advancements in smart infrastructure, energy efficiency regulations, and growing adoption of electric vehicles.

In 2024, Latin America accounted for a share of 7% of global ambient light sensors market. The high adoption of ambient light sensors in precision agriculture is a major factor growth of ambient light sensors in the region.

Brazil ambient light sensors market is expected to grow at a CAGR of 6.7% during the forecast period. The growth of ambient light sensors market in Brazil is attributed to the growth of precision farming solutions improving light regulation for better crop yield and reducing energy consumption.

Mexico ambient light sensors market is expected to grow at a CAGR of 8% during the forecast period. The growth of ambient light market in Mexico is attributed to increasingly adopting smart city initiatives. The authorities in Mexico are integrating ambient light sensors in street lights to reduce energy consumption and enhance sustainability.

In 2024, Middle East and Africa accounted for a share of 9% of global ambient light sensor market. The increased push towards sustainability and energy efficiency and automation in public infrastructure are major factors driving market growth.

In 2024, UAE accounted for 45.9% of the Middle East & Africa ambient light sensors market. The growth of UAE ambient light sensors market is driven by the government’s pursuit to become global leader in smart cities, energy-efficient technologies, and sustainable development.

Saudi Arabia ambient light sensors market is expected to grow at a CAGR of 8.9% during the forecast period. Saudi Arabia ambient light sensors is driven by Saudi Green Initiatives aiming to reduce carbon emissions and increasing energy efficiency. The adoption of ALS for enhancing lighting automation in public infrastructure supports the government’s energy efficiency targets, driving the market growth.

South Africa ambient light sensors market will reach USD 17 million by 2034. The growing adoption of ambient light sensors in digital signages in retail and advertising sector is driving the market growth in South Africa during the forecast period.

Ambient Light Sensor Market Share

The ambient light sensors market is competitive and highly fragmented with the presence of established global players as well as local players and startups. The top 5 companies in the global ambient light market are ams-OSRAM AG, Melexis NV, ON Semiconductor corporation, Sharp corporation, and ROHM semiconductor, collectively accounting for a share of 35%. These companies are competing in the market by offering advanced sensors that enhance energy efficiency and seamlessly interact with IoT devices. For instance, In June 2024, Melexis, a manufacturer of automotive LED drivers for ambient lighting, announced the extension of its LIN RGB product portfoilio with the MLX81123. In sleep mode, the MLX81123 exhibits a typical standby current consumption of just 25 µA and features a 28 V jump start. The operating temperature is a wide -40°C to +125°C with a built-in temperature sensor for thermal monitoring, ideal for even the most demanding automotive applications.

New product launches is the most significant strategic development which key players in the market are adopting for augmenting their market share. Key ambient light sensor manufacturers are increasingly launching new products for proliferation in automotive sectors. For instance in 2023, ams-OSRAM AG launched OSIRE® E3731i LED with intelligent ambient light sensing capabilities for integration into next-generation passenger vehicles. The company also created a new Open System Protocol (OSP), a ‘language’ that enables compatible devices such as LEDs, microcontrollers and sensors to talk to each other over a standard serial bus. The OSP is free for any manufacturer to use, helping to foster a vibrant ecosystem of products and suppliers to support auto OEMs technological development initiatives in the area of ambient lighting.

ams-OSRAM AG provides ambient light sensors which accurately measures the intensity of ambient light and matches it with the human eye response to light. ams-OSRAM AG competes in the market by doing strategic partnerships with the leading automotive OEMs. For instance, in December 2024, OSRAM partnered with Valeo to develop ambient lighting systems comprising optics, electronics and software enabling RGB ambient lighting with high optical homogeneity and color accuracy, while ensuring smooth light animation throughout the vehicle cabin.

Melexis NV primarily competes in the market with their rapid product development, keeping pace with the customer demands and evolving industry needs.

ON Semiconductor provides a wide range of ambient light sensing products for various applications. Such vast product portfolio enables On Semiconductor to command a leading position in the market.

Ambient Light Sensor Market Companies

Top 5 companies operating in the ambient light sensor industry are:

ams-OSRAM AG

Melexis NV

ON Semiconductor Corporation

ROHM Semiconductor

Sharp Corporation

Ambient Light Sensor Industry News

In April 2024, Ams OSRAM collaborated with Malaysia’s DOMINANT Opto Technologies to integrate the OSP (Open System Protocol) into next-generation intelligent RGB LEDs for automotive ambient lighting. This collaboration further strengthens innovation and ensures technology compatibility in the automotive lighting industry.

In June 2024, HaiLa announced the company’s partnership with e-peas on a battery-free wi-fi backscatter system powered by ambient light. The key objective of the this collaboration of new potential to run autonomous Wi-Fi devices free of disposable battery and maintenance needs.

This ambient light sensor market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Million) & (Volume Unit) from 2021 to 2034, for the following segments:

Market, By Sensor Type

Photodiode-based

CMOS-based

Infrared-based

Market, By Output Type

Analog

Digital

Market, By Mounting Style

SMD/SMT

Through hole

Others

Market, By Integration

Discrete

Combination

Market, By Application

Consumer electronics

Automotive

Industrial

Home automation

Healthcare

Entertainment

Security

Others

The above information is provided for the following regions and countries:

North America

U.S.

Canada

Europe

UK

Germany

France

Italy

Spain

Russia

Asia Pacific

China

India

Japan

South Korea

ANZ

Latin America

Brazil

Mexico

MEA

UAE

Saudi Arabia

South Africa

環境光センサー業界ニュース

2024年4月、アムス・オスラムはマレーシアのDOMINANT Opto Technologies社と協業し、車載用環境照明の次世代インテリジェントRGB LEDにOSP(オープン・システム・プロトコル)を統合しました。この協業により、イノベーションがさらに強化され、自動車照明業界における技術の互換性が確保されます。

2024年6月、HaiLaはe-peasと、環境光で駆動するバッテリーフリーのWi-Fiバックスキャッターシステムに関する提携を発表しました。この提携の主な目的は、使い捨てバッテリーとメンテナンスの必要性から解放された自律型Wi-Fi装置を稼働させる新たな可能性です。

この調査レポートは、環境光センサー市場を詳細に調査し、2021年から2034年までの収益(百万米ドル)および(台数単位)の推計と予測を掲載しています:

市場:センサ種類別

フォトダイオードベース

CMOSベース

赤外線ベース

市場:出力種類別

アナログ

デジタル

実装スタイル別市場

SMD/SMT

スルーホール

その他

統合別市場

ディスクリート

コンビネーション

アプリケーション別市場

電子機器

自動車

産業用

ホームオートメーション

ヘルスケア

エンターテイメント

セキュリティ

その他

上記の情報は、以下の地域および国について提供されています:

北米

アメリカ

カナダ

ヨーロッパ

英国

ドイツ

フランス

イタリア

スペイン

ロシア

アジア太平洋

中国

インド

日本

韓国

ニュージーランド

ラテンアメリカ

ブラジル

メキシコ

中東・アフリカ

UAE

サウジアラビア

南アフリカ

第1章 方法論と範囲

1.1 市場範囲と定義

1.2 基本推計と計算

1.3 予測計算

1.4 データソース

1.4.1 一次データ

1.4.2 セカンダリー

1.4.2.1 有料ソース

1.4.2.2 公的情報源

第2章 エグゼクティブサマリー

2.1 産業の概要、2021-2034年

第3章 業界インサイト

3.1 業界エコシステム分析

3.1.1 バリューチェーンに影響を与える要因

3.1.2 利益率分析

3.1.3 混乱

3.1.4 将来展望

3.1.5 メーカー

3.1.6 ディストリビューター

3.2 サプライヤーの状況

3.3 利益率分析

3.4 主なニュースと取り組み

3.5 規制の状況

3.6 影響力

3.6.1 成長ドライバー

3.6.1.1 家電製品への統合の増加

3.6.1.2 スマートホーム技術の進歩

3.6.1.3 ヘルスケア・アプリケーションの拡大

3.6.1.4 エネルギー効率に対する意識の高まり

3.6.2 業界の落とし穴と課題

3.6.2.1 先端センサー技術のコスト高

3.6.2.2 新興国における認知度の低さ

3.7 成長可能性分析

3.8 ポーター分析

3.9 PESTEL分析

第4章 競争環境(2024年

4.1 はじめに

4.2 各社の市場シェア分析

4.3 競合のポジショニング・マトリックス

4.4 戦略的展望マトリクス

第5章 2021~2034年センサー種類別市場予測(百万米ドル・単位)

5.1 主要トレンド

5.2 フォトダイオードベース

5.3 CMOSベース

5.4 赤外線ベース

第6章 2021~2034年、出力種類別市場予測・予測(百万米ドル・単位)

6.1 主要トレンド

6.2 アナログ

6.3 デジタル

第7章 2021〜2034年マウントスタイル別市場規模予測・予測(百万米ドル・台数)

7.1 主要動向

7.2 SMD/SMT

7.3 スルーホール

7.4 その他

第8章 2021年~2034年集積度別市場予測・展望(百万米ドル・単位)

8.1 主要動向

8.2 ディスクリート

8.3 コンビネーション

第9章 2021-2034年アプリケーション別市場規模予測・予測(百万米ドル・台数)

9.1 主要動向

9.2 民生用電子機器

9.3 自動車

9.4 産業用

9.5 ホームオートメーション

9.6 ヘルスケア

9.7 エンターテインメント

9.8 セキュリティ

9.9 その他

第10章 2021〜2034年地域別市場予測(百万米ドル・単位)

10.1 主要動向

10.2 北米

10.2.1 アメリカ

10.2.2 カナダ

10.3 ヨーロッパ

10.3.1 イギリス

10.3.2 ドイツ

10.3.3 フランス

10.3.4 イタリア

10.3.5 スペイン

10.3.6 ロシア

10.4 アジア太平洋

10.4.1 中国

10.4.2 インド

10.4.3 日本

10.4.4 韓国

10.4.5 オーストラリア

10.5 ラテンアメリカ

10.5.1 ブラジル

10.5.2 メキシコ

10.6 MEA

10.6.1 南アフリカ

10.6.2 サウジアラビア

10.6.3 アラブ首長国連邦

第11章 企業プロフィール

11.1 Analog Devices (Maxim Integrated)

11.2 ams-OSRAM AG

11.3 Broadcom Inc.

11.4 Everlight Electronics Co., Ltd.

11.5 Honeywell International Inc.

11.6 Melexis NV

11.7 Microchip Technology Inc.

11.8 OmniVision Technologies, Inc.

11.9 ON Semiconductor Corporation

11.10 Panasonic Corporation

11.11 Renesas Electronics Corporation

11.12 ROHM Semiconductor

11.13 Samsung Electronics Co., Ltd.

11.14 Sharp Corporation

11.15 Silicon Labs

11.16 Sony Semiconductor Solutions Corporation

11.17 STMicroelectronics

11.18 Texas Instruments Incorporated

11.19 Vishay Intertechnology

*** 本調査レポートに関するお問い合わせ ***